CHARTS: US copper glut hides refining crunch

AI Analysis

The copper processing deficit represents a strategic vulnerability for U.S. manufacturing. Investments in domestic refining could unlock significant economic and geopolitical advantages in critical minerals infrastructure.

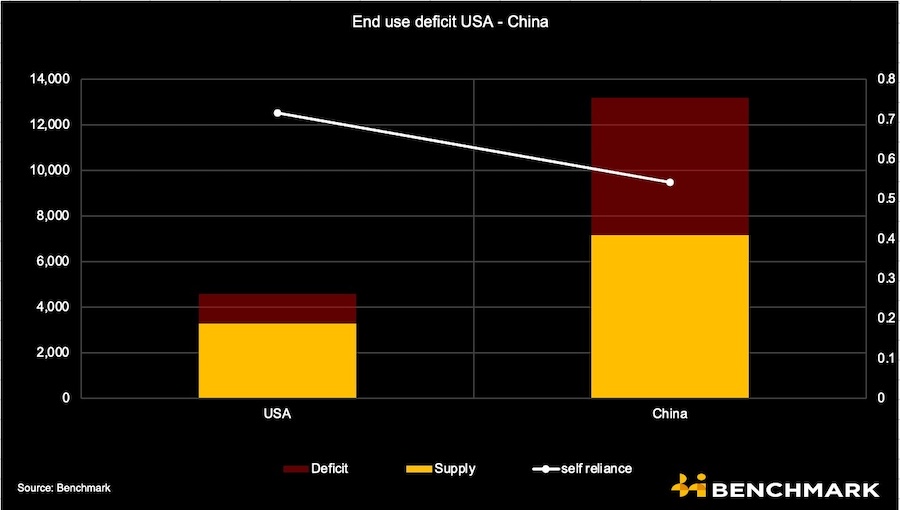

A critical bottleneck in the U.S. copper supply chain is emerging, with domestic mining output far outpacing the nation's ability to process raw materials into refined metal. According to Benchmark Mineral Intelligence, the United States produces enough copper to meet 146% of its domestic demand, yet remains paradoxically dependent on foreign refiners to convert concentrate into usable industrial copper.

The data reveals a stark structural challenge: while U.S. copper mines generated 1,714 kilotonnes in 2024, nearly 48% of mined copper concentrate is exported, primarily due to limited domestic smelting and refining capabilities. This means American manufacturers must often rely on international processors, particularly in China, to transform raw copper into refined cathodes.

Benchmark's copper analyst Albert Mackenzie underscored the strategic implications, noting that the U.S. is far more self-reliant in raw copper production compared to China, but lacks the downstream processing infrastructure to fully capitalize on this advantage. The key constraint remains conversion capacity, not mining output.

For precious metals investors, this presents a nuanced opportunity. Expanding domestic refining infrastructure could potentially reduce reliance on foreign processors, create new industrial investment channels, and strengthen U.S. supply chain resilience in critical metals.

The report suggests that strategic investments in processing technology and facilities could transform this current limitation into a significant competitive advantage, potentially reshaping global copper trade dynamics in the coming decade.

Key Takeaways

- US produces 146% of copper demand, but lacks refining capacity

- 48% of copper concentrate is exported for foreign processing

- Domestic infrastructure investments could resolve supply chain weakness

- Potential opportunity for strategic metals investors